Click here to read the original Cautious Optimism Facebook post with comments

"The [debtors'] prison is full of the most reputable merchants, and it is understood that the scene is not yet got to its height.”

-Letter from Vice President Thomas Jefferson to President John Adams, 1798

8 MIN READ - The Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff continues with the history of America’s very heavily regulated and very crisis-prone banking system—this time examining how its first privileged central bank—the Bank of the United States—precipitated the Panic of 1797.

|

| Alexander

Hamilton’s Bank of the United States produces another banking panic and depression in 1797 |

As we discussed in the previous column on the Panic of 1792, U.S. Treasury Secretary Alexander Hamilton’s Bank of the United States (BUS) opened for business in 1791 and immediately began aggressive lending and moneyprinting operations to support a large federal debt and spur industry.

The inflation created a major speculative bubble in U.S. Treasury bonds and shares of the BUS itself that collapsed in 1792, bankrupting many speculators and forcing Hamilton to use government money to prop up bond market prices, make emergency bailout loans to distressed institutions, and guarantee loans made by solvent banks.

The Panic of 1792 subsided quickly and the U.S. avoided a protracted recession with growth returning in 1793.

One would hope Hamilton would have learned lessons in 1792 about the dangers of aggressive money creation, but he returned to inflation in 1793, his BUS raising prices for several years and blowing another speculative asset bubble that burst in 1797.

VIII. THE DANGER OF THE BUS’S LEGAL PRIVILEGES

To understand how the BUS alone could wreak so much havoc on the U.S. economy, it’s important to understand its unique structure at the time.

The BUS was not as powerful as modern central banks like the Federal Reserve. Under the nation’s bimetallic silver and gold standard it did not have the ability to issue fiat money without limit. It still had to make good on its pledge to redeem its banknotes in specie, and it did not have a monopoly on paper currency since America’s private banks were also issuers of banknotes.

But the BUS was by far the largest company in the country and its special connection to the federal government gave it far more influence over the economy than any other private bank.

Not only was the government a 20% owner in the Bank itself—aligning their mutual interests as Hamilton intended—it also bestowed certain unique legal privileges upon the BUS that contributed to its outsized influence.

1) Unlike other private banks, the federal government announced it would only accept BUS banknotes for payment of excise taxes, thus giving them a quasi-legal tender status and guaranteeing their ubiquitous circulation.

2) The BUS was selected as the federal government’s exclusive bank of deposit for Treasury funds, not surprising given Hamilton was Secretary of the Treasury. As caretaker of all federal funds the BUS was thus bestowed with outsized public prestige.

3) As sole bank of deposit for federal funds, the BUS gained an unofficial “too big to fail” status with the public. Everyone knew there was no way the federal government would allow its own bank to fail, taking its 20% stake and all federal deposits down with it. Hence the BUS attracted a large business for private retail and commercial deposits and enormous control over the nation’s money supply and credit policy.

4) Finally the BUS was given an exclusive monopoly on interstate branching. State-level unit banking laws, which we’ve discussed in previous articles on American banking, prohibited any private bank from branching outside its home state, and many states prohibited branching outside a small region or forbade branching at all. The federal government allowed the BUS to branch anywhere it wanted, hence spreading its reach and influence nationwide.

Given the dominant and nationwide circulation of its currency alongside the prestige of being the government’s bank of deposit, BUS banknotes were treated by private banks as a reserve asset themselves. Since a smaller share of its notes were submitted for redemption and instead held in reserve at other institutions, the BUS engaged in greater leverage and could issue far more currency than other private banks.

All these privileges granted to the BUS, and denied to competing private banks, made it an incredibly powerful institution posing an outsized risk to the economy.

In a free, competitive system with many private banks, if one bank errs and issues too much paper or deposit money it disproportionately suffers the consequences. But as we shall see Hamilton’s mistakes during the mid-1790’s inflicted injury upon the entire nation.

IX. THE BOOM OF THE 1790’S

After the Panic of 1792 subsided Hamilton restarted his issuances of loans, printed vast quantities of new BUS banknotes and expanded demand deposits. The result was a multiyear price boom with consumer price index inflation hitting double digits in 1794 and 1795 (Officer).

Wholesale prices rose 17-18% in 1793 and incredibly by over 50% in 1795 before collapsing in 1796 (U.S. Dept. of Commerce). Such inflation rates are astounding considering the U.S. was on a combined gold/silver standard at the time.

Furthermore BUS easy money and credit artificially drove down interest rates, fueling a craze of business startups and wild land speculation with many of the country’s top financiers joining in the frenzy.

Hamilton’s own mentor and former Bank of North America president Robert Morris raised $10 million with investment partners for business and land ventures, an enormous figure considering the federal government’s annual budget was only $8 million in 1795.

A mania for transportation (canal and turnpike) companies began with firms popping up such as the Lancaster Turnpike Company and Robert Morris’ Schuylkill & Susquehanna [Rivers] Company.

Hamilton’s father-in-law, American Revolution General and former New York Senator Philip Schulyer, used low-interest loans to found the Western Inland [Lock] Navigation and Northern Inland Lock Navigation Companies.

Both Morris’ and Schulyer’s companies would go bankrupt in the ensuing depression.

And with so much easy money circulating a wave of new bank startups began. The number of private American banks is estimated to have nearly doubled from 12 in 1792 to 22 in 1796.

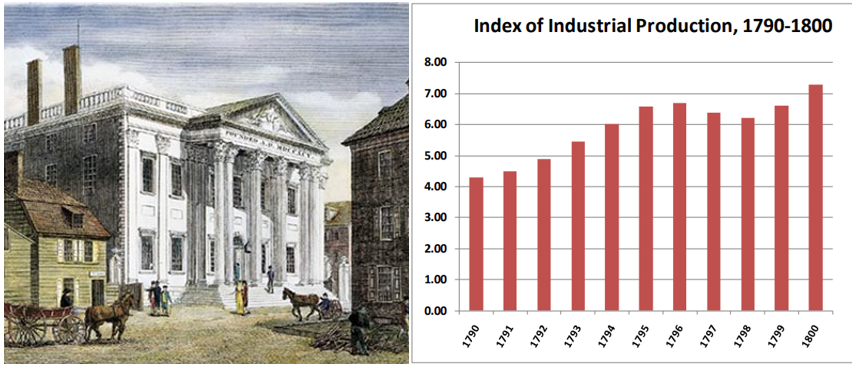

Despite the dangerous buildup of asset bubbles, everyday Americans initially viewed the mid 1790’s as a benign boom period of riches, just as other central bank induced bubbles have cast similar illusions of perpetual prosperity. Real per capita GDP rose 5.7% annually from 1792 to 1795 and industrial production rose 8.1% per year.

X. THE PANIC AND DEPRESSION OF 1797

Unsurprisingly the boom proved to be illusory when the BUS was abruptly forced to stop issuing credit in 1796. Not only were its notes overextended leading to increasing domestic calls for specie redemption, but price inflation also produced a gold drain from America to Europe via the price-specie flow mechanism.

Under an international gold standard, if the U.S. produces too many paper money claims and prices rise, imports appear cheaper in gold terms and both its own and international consumers shift to buying cheaper overseas goods over inflated American ones. The inevitable result is a trade deficit for the U.S. resulting in net outflows of gold as the notes Americans use to buy imports are retuned from abroad for gold redemption.

The Economics Correspondent has written in more detail on the price-specie flow mechanism at:

http://www.cautiouseconomics.com/2018/11/the-great-depression-01.html

(see section II)

As the BUS saw its gold reserves dwindling due to overseas redemption calls, it quickly halted new loans and called in existing ones to save itself, effectively contracting the money supply in a classic credit crunch. Starved of new money, asset bubbles began to burst across the country ruining speculators, many of whom had leveraged themselves to join in the investment schemes.

By 1796 deflation had set in. Businesses could not obtain new loans while their revenues fell in concert with prices, and failures began en masse later that year. By early 1797 the United States was in full blown recession (called “depression” before World War II).

Incidentally some economists theorize that the Panic and Depression of 1797 were not endogenous events but rather the catalyst was the Bank of England’s suspension of gold payments at the onset of the Napoleonic Wars.

Undoubtedly Great Britain calling in gold redemption and then hoarding gold from the world would have made the depression worse, but the Bank of England suspension began on February 27, 1797 while deflation and mass business failures already plagued America by late 1796. It's therefore difficult to see how America’s 1797 slump could have originated with Britain’s suspension of the gold standard.

Nevertheless the best historical records available indicate U.S. GDP turned decisively negative from 1796 to 1797.

Retail CPI fell approximately 3% from 1796 to 1797 and again the following year.

Wholesale prices fell an astounding 30% from 1796 to 1797, reflecting a particularly harsh retrenchment in industry.

The index of industrial production fell approximately 7.3% from 1796 to 1798 which is somewhat comparable to the 8.3% decline America endured during the Paul Volcker Fed recession of 1981-1983.

On the ground widespread business foreclosures and factories that had sprung up only a few short years prior now lay empty ghost towns dotted throughout America’s largest cities.

And speculators were ruined. Robert Morris and his partner John Nicholson—two of America’s wealthiest men—went to debtors’ prison.

Supreme Court Justice James Wilson was brought down by bad land deals and spent time in debtors’ prison. From jail he continued his legal duties as bad debts were not among the criteria listed for removal from the Court.

They were hardly alone as financiers across the nation lost fortunes. Vice President Thomas Jefferson noted in an early 1798 letter to President John Adams that “the prison is full of the most reputable merchants, and it is understood that the scene is not yet got to its height.”

In fact so many investors were ruined that the depression led to creation of the Federal Bankruptcy Act of 1800 to give petition to insolvent debtors.

1797 delivered the young republic its first truly nationwide depression, and its roots can be traced to the late 18th century version of what economists today recognize as a central bank-induced easy money speculative bubble.

Economic conditions bottomed out in 1798 and growth resumed late in the year. However, the damage to the BUS’s reputation was already done. Americans adopted a suspicious view of the bank, and the anguish of two financial panics in a single decade triggered the creation of a new political party, the Jeffersonian Democratic Republican Party, serving as a counterweight to the power of the Hamiltonian Federalists.

It was, after all, Thomas Jefferson himself who opposed the Bank of the United States and warned of its dangers back in 1791.

Alexander Hamilton had already resigned as Treasury Secretary in 1795 to focus on private law and finance including BUS operations. After weathering America’s first political sex scandal in 1797 he attempted to exert influence during the John Adams presidency of 1797-1801 and was later killed in the famous duel with Aaron Burr.

His Bank of the United States would not get another chance to create more asset bubbles and depressions before failing to win renewal of its charter in 1811. The Senate vote deadlocked in a tie and Vice President George Clinton voted against renewing the charter.

But the BUS would have a successor, the Second Bank of the United States, which picked up where Hamilton left off with a new charter in 1816.

For those who wish to know more about the Panic and Depression of 1797, Curott and Watts have an excellent Johns Hopkins paper available at:

https://sites.krieger.jhu.edu/iae/files/2017/04/Curott_Watts_Recession_of_1797.pdf

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.