Click here to read the original Cautious Optimism Facebook post with comments

2 MIN READ - The Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff posts an update on the Federal Reserve’s ballooning interest on reserves payments to commercial banks, which are approaching $160 billion this year.

|

| Click to enlarge |

The Fed’s yearlong campaign of interest rate hikes has dominated financial news headlines for some time now, but buried deep in the Fed’s latest quarterly report is a little-reported yet huge offshoot of its rapid tightening policy.

The Fed is on track to pay U.S. commercial banks over $160 billion in risk-free interest payments in 2023.

But before CO Nation harps on the banks, it’s worth noting the payments are the result of three major monetary policy shifts, all championed by the Fed itself.

1) Even since 2008 the Fed has conducted monetary policy on a “floor system” where it creates trillions of dollars in new reserves to buy assets from banks, but pays them interest to sequester those reserves and discourages them from lending aggressively which would make inflation far worse than it already is.

2) Instead of reducing its balance sheet as it tried from 2015 to 2019, the Fed ballooned it again in early 2020 as a response to the Covid pandemic. So instead of paying interest on $1.5 trillion in banking system reserves in September 2019, the Fed now finds itself paying interest on $3.2 trillion in reserves today.

3) Lastly, paying interest even on $3.2 trillion in reserves may not have been a big deal when the Fed’s “interest on reserves” policy rate was only 0.15% in early 2022. But over the last year the Fed has completed its Bermuda Triangle trifecta by rapidly hiking the interest on reserves rate to 5.15% as of this writing, and it’s likely to climb even further after the Federal Open Market Committee’s July 25th meeting.

Anyone with a calculator who understands Fed policy can estimate paying an interest on reserves rate of 5.15% on $3.2 trillion will equal a windfall for the commercial banks (about $160 billion), but nothing confirms it more than the Fed’s own quarterly income statement.

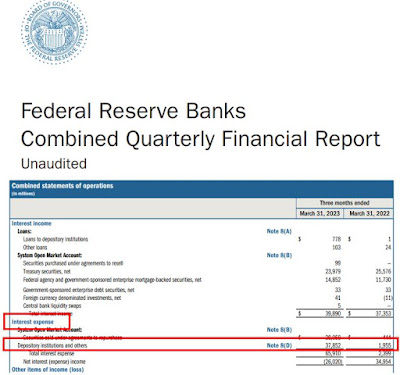

Scanning the Fed’s finances under expenses (picture attached) the Fed’s Q1 interest on reserves payments to banks is denoted as “Interest Expense: Depository Institutions and Others.”

Amount paid? $37.852 billion vs. just $1.955 billion a year ago.

Also keep in mind these numbers reflect the first quarter of 2023 (Jan 1-Mar 31) when the interest on reserves policy rate sat anywhere from 4.4% to 4.9%. Now that it’s up to 5.15%, and going even higher soon, subsequent interest payments will be that much greater.

And that translates to a bottom line of more than $160 billion in risk-free, zero maturity interest for U.S. commercial banks by the time 2023 is over.

The Economics Correspondent isn’t particularly on the bash-the-banks bandwagon and doesn’t blame them for the current arrangement. Rather, the floor system and payment of interest on reserves was entirely the brainchild of academic theorists at the Fed who lobbied Congress hard for authority to implement their new operating system in the mid 2000’s.

Even when they put it into action during the 2008 financial crisis, the interest on excess reserves rate was 0.25% on $1.1 trillion of reserves in late 2009 (just $2.75 billion per year in payments) and 0.25% on a peak $2.84 trillion of reserves in 2015 (still only $6.9 billion per year).

But as of 2022 the Fed has really screwed the pooch ballooning system reserves to $4.2 trillion in 2022 and struggling to bring it down to $3.2 trillion today, all while dropping the ball on inflation and being forced to raise the interest on reserves rate to 5.15% and climbing.

Data source links:

1) Federal Reserve 1Q2023 quarterly financial report (page 3 for interest expense).

https://www.federalreserve.gov/aboutthefed/files/quarterly-report-20230609.pdf

2) Reserves of depository institutions.

https://fred.stlouisfed.org/series/TOTRESNS

3) Interest on reserves rate (July 2021 to present).

https://fred.stlouisfed.org/series/IORB

4) Interest on excess reserves rate (October 2008 to July 2021).

https://fred.stlouisfed.org/graph/?g=16YdX