10 MIN READ - An important in depth analysis from the Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff

|

| Real federal spending nearly doubles 1929-1933 |

This month we focus on the historical lesson of government

spending (more or less?) during an economic slump—the correlative to last

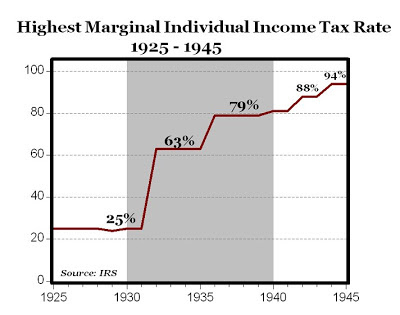

month’s discussion on Herbert Hoover’s destructive 1932 tax hike (from a top

marginal rate of 25% to 63%) and FDR’s nearly equally detrimental 1936 increase

from 63% to 79% and new “undistributed profits” tax.

Mainstream Great Depression histories and the economics columns of America’s major newspapers have been mostly silent on Hoover’s massive revenue measures that sent the economy plunging to its worst levels in American history the following year—opting instead to criticize his laissez-faire approach. But what have they said about spending?

I. ECONOMIC FAIRY TALES: HERBERT HOOVER WAS A BUDGET-SLASHING AUSTERIAN

Well Herbert Hoover’s 1929-1933 spending policy is one subject the press and academia were certainly not silent on. During the Great Recession the New York Times, Washington Post, Boston Globe, the Guardian, Atlantic, and other more liberal outlets like Salon, Slate, Vox, Huffington Post, etc… were virtually unanimous in their endless bemoaning of government austerity—primarily in Europe—and repeatedly cited their own “lessons” from the Great Depression: that Herbert Hoover slashed federal spending at a time when the economy needed expansionary stimulus in the form of enlarged budgets and fiscal deficits. The examples are virtually endless, but here are just a few to illustrate:

“The nation will be reeling from the actions of 50 Herbert Hoovers — state governors who are slashing spending in a time of recession”

-Paul Krugman, “Fifty Herbert Hoovers,” New York Times, Dec 28, 2008

“Virtually all the deterioration in the US debt position from 1929 to 1939 took place under the tight-fisted Hoover rather than under FDR… …the Hoover experience also provides a nice illustration of self-defeating austerity… …It’s too bad that people who don’t understand any of that seem to have the upper hand in policy.”

-Paul Krugman, “Debt Depression,” New York Times, July 20, 2010

“World Leaders Heed Herbert Hoover, Opt for Belt-Tightening Over Economic Stimulus”

-CBS News, June 7, 2010

“[Nobel Laureate economist Joseph] Stiglitz believes the world is in danger of repeating U.S. President Herbert Hoover's mistakes in 1929 of slashing spending. ‘There is ample evidence on this,’ Stiglitz said. ‘We call these Hooverite policies (government austerity measures) in honor of Herbert Hoover.’”

-CNN, “Depression, Double-Dip, and Deficits: Economists Speak Out,” July 9, 2010

“But one of the most basic principles of economics is that when an economy is anemic, governments should use deficit spending as a fiscal stimulus, even though that means an increase in debt. If Senator Rubio believes that the response to a weak economy is to slash spending, he is embracing the approach that Herbert Hoover discredited 80 years ago.”

-Nicholas Kristof, “Why Pay Congress?”, New York Times, April 6, 2011

“That‘s a bad thing. Hoover is a political epithet in bad economic times because his response to the depression—was to, first do nothing and then do stuff that made it worse. The country needed massive federal spending to stimulate demand and keep people working. Hoover? Cut spending… …I‘m Herbert Hoover. I can‘t do anything helpful. How about I hurt the economy some more instead because of my dumb, moralistic, ideologically-driven, ignorant, short-term, self-serving bad ideas? I‘ll take this depression and make it not just good but great. That‘s the ticket, the Great Depression.”

-Rachel Maddow, “The Rachel Maddow Show,” December 12, 2008

Regarding the Maddow quote: to anyone who knows anything

about government spending under the Hoover administration, you can only shake

your head in disbelief at the awesome ignorance of such a self-righteous

commentary. OK I know, Rachel Maddow is no economist. She’s not even a good

economics commentator. But she did at least get the part right about Herbert

Hoover turning a recession that started in 1929 into the Great Depression.

But for the opposite reason. Herbert Hoover was actually a runaway spender. As you’ll see it’s not even up for debate.

II. THE NEW YORK TIMES VS. ECONOMIC HISTORY, HERBERT HOOVER: PROFLIGATE SPENDTHRIFT

Which leads us away from the New York Times, CBS, CNN, and Rachel Maddow back to economic reality on planet Earth. Since Krugman, Stiglitz, Kristof, or Maddow have for good reason never produced any actual 1930’s budget numbers to back up their assertions, let's discuss the important details that they never will:

1) In response to the 1929 stock market crash, Herbert Hoover launched the largest peacetime percentage expansion of federal spending in American history—then or ever since. From Calvin Coolidge’s last budget (FY29) to Hoover’s last budget (FY33), federal spending rose 47% from $3.127 billion to $4.598 billion (source: whitehouse.gov historical budget tables—although any 1930’s budget source will confirm the same).

https://www.usgovernmentspending.com/spending_chart_1929_1933USk_20s2li111mcn_F0f

2) But that’s just the beginning. During the same 1929-1933 period rapid deflation boosted the dollar’s purchasing power due to the failure of nearly 10,000 commercial banks and credit contraction by highly stressed surviving banks. The money supply fell by nearly a third as did prices. So an inflation-adjusted dollar spent in 1933 was worth almost 1.5 times its 1929 value. Adjusting Hoover’s FY33 budget for deflation, spending swelled by 93.5% in real terms. In fact, calculating the hike from the nadir of the monetary contraction in the late spring of 1933 federal spending rose briefly by over 100%. Yes, you read that correctly. Herbert Hoover nearly doubled real government spending. Not quite the “draconian cuts” you may have read about?

https://www.usgovernmentspending.com/spending_chart_1929_1933USk_19s2li111lcn_F0f_Recent_Federal_Spending_In_Percent_GDP

3) As if it couldn’t get any worse, as a percent of GDP

federal spending rose from 3.64% to 8.92%--due to a combination of real

spending hikes and the shrinking economy. So as a share of the economy, Herbert

Hoover ballooned federal spending by 145% or to about 2.5 times its original

size.

https://www.usgovernmentspending.com/spending_chart_1929_1933USp_19s2li111lcn_F0f_Recent_Federal_Spending_In_Percent_GDP

https://www.usgovernmentspending.com/spending_chart_1929_1933USp_19s2li111lcn_F0f_Recent_Federal_Spending_In_Percent_GDP

On a side note Keynesian economists argue “You can’t measure

federal spending as a percent of GDP because the economy was collapsing from

1929-1933 which distorts the calculation. It’s an unfair metric.” To which

there are at least two valid responses: First, even ignoring government

spending as a share of GDP, real spending itself nearly doubled which is

already high enough to kill the “austerity” myth. But second, Keynesians always

argue huge boosts in government spending are precisely what prevent

recessions/depressions from getting worse in the first place. So if Herbert

Hoover oversaw the largest peacetime spending expansion in American history,

why was the economy even collapsing? Shouldn’t his near-doubling of real

government spending have saved America, or at least prevented the calamity of

the Great Depression instead of delivering… well, the Great Depression?

Or is it just possible that there's something wrong with their theory, and that all this profligate government spending is precisely what made things worse? The data sure fits the alternate theory a lot better than theirs.

Or is it just possible that there's something wrong with their theory, and that all this profligate government spending is precisely what made things worse? The data sure fits the alternate theory a lot better than theirs.

Incidentally, if we account for all levels of government and include state and local spending—the hike as a share of GDP, while still enormous, wasn’t quite as dramatic: up “only” 98%. But other than some aid to state and local governments, Herbert Hoover had much less of an effect on their budgets than Washington’s. And of course the main target of the media’s Great Recession criticism was Hoover’s austerity, not the states'. But the evidence that total government spending at all levels by 1933 had doubled up to 22% of GDP also establishes that government spending was by no means insignificant by then, and was in fact a record at the time. By contrast, during America’s second worst depression, the Depression of 1893, total spending at all levels of government tallied at only 7-8% of GDP. And not coincidentally the Depression of 1893 ended in less than half the time as the Great Depression.

https://www.usgovernmentspending.com/spending_chart_1929_1933USp_11s0li111lcn_F0t_US_Government_Spending_As_Percent_Of_GDP

4) When confronted with the folly of austerity claims—a rare occasion in and of itself—Keynesian economists will sometimes focus on a single year: FY33 where federal spending dipped slightly from the previous year—from $4.659 billion to $4.598 billion, a decline of 1.3%.

But to call a 1.3% cut “draconian” or characterize it as “slashing spending” is not only an anemic argument, it once again ignores the impact of deflation. One dollar in 1932 was worth $1.11 in 1933, so in 1932 dollars the FY33 budget was not $4.598 billion but instead $5.104 billion, yet another hike—this time up 9.6% in real terms. Pointing to FY33 as the year of tragic austerity is just a fool’s errand.

5) One more legend of Hooverian austerity is his Treasury Secretary Andrew Mellon’s advice in the early days of the downturn to “Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate…” which Hoover has recounted in his memoirs (available online at the Hoover Institution). Paul Krugman has also resurrected the quote in his April 2011 column “The Mellon Doctrine”—the insinuation being that Mellon’s quote is proof that Hoover stood by and allowed the economy to collapse in the mistaken belief that liquidation and adjustment were the proper policy response.

Well if only Hoover had really believed that. Americans might have been spared a lot of pain and suffering! The problem is two paragraphs later in the same memoirs Hoover describes his reaction to Mellon—which unsurprisingly Krugman, Delong, Stiglitz and others have chosen not to tell their readers about:

“Secretary Mellon was not hard-hearted. In fact he was generous and sympathetic with all suffering. He felt there would be less suffering if his course were pursued… ...But other members of the Administration, also having economic responsibilities—Under Secretary of the Treasury Mills, Governor Young of the Reserve Board, Secretary of Commerce Lamont and Secretary of Agriculture Hyde—believed with me that we should use the powers of government to cushion the situation… …The record will show that we went into action within ten days and were steadily organizing each week and month thereafter to meet the changing tides— mostly for the worse. In this earlier stage we determined that the Federal government should use all of its powers.”

-Hoover memoirs, p. 316) Finally the last demand-side line of defense usually goes something like “Well, Hoover tried but his spending programs weren’t big enough” and the standard corollary of “The Great Depression would have been worse were it not for his half-measures.” Of course every time the Keynesian prescription has all-too-often failed (think Obama’s $800 billion 2009 ARARA stimulus, bloated European budgets in the initial post-2008 crisis years, and multiple Japanese stimulus packages) the “not big enough” card is dusted off and played, almost as if on an automated script.

But America experienced major depressions in 1837, 1873, 1893, 1907, and 1920, the first four in particular with major financial/banking panics. Not only were federal stimulus spending programs “not big enough” then either, they were completely nonexistent since demand-side economic policies hadn’t been invented yet. In fact, the federal government’s standard response prior to 1929 was to cut the budget during slumps to compensate for falling tax revenues.

According to the Paul Krugmans of the world, those downturns should have deteriorated into “Greater Great Depressions,” lasting entire generations. But the opposite happened: the slumps were over in a year or two and full employment was restored in anywhere from two years (Depression of 1907 and 1920) to at most seven (Depressions of 1873 and 1893), instead of the eleven years required after 1929, or more accurately sixteen years if you exclude World War II when the US military conscripted 12 million men, sent them overseas, and counted them as “employed.”

It’s also worth noting that early 1930’s federal spending increases were not on liberal bête noires like military budgets, but rather for standard New Deal type programs: The Resolution Finance Corporation to bail out railroads, politically connected banks and businesses. Compensation to state governments for falling tax revenues. The Federal Farm Board to buy up crops in an attempt to prop up produce and livestock prices, and eventually pay farmers directly to stop growing food. Public works programs building roads, bridges, parks, buildings and large jobs projects such as Mount Rushmore and the Hoover Dam. So no one can argue Hoover’s budgets weren’t “demand boosting” in the longstanding conventional sense.

III. WHERE RECORD TAX AND SPENDING HIKES GOT US (AND WILL STILL GET US NEXT RECESSION)

But back to what we now know is, to borrow a line from economist Lawrence Reed, one of the Great Myths of the Great Depression: that Herbert Hoover was a tight-fisted budget cutter. The countless claims in America’s newspapers and among academics that Hoover was a small government austerian is an openly categorical falsehood. Herbert Hoover launched tax hikes and spending increases that, measured as percentage gains, were and still remain records for American peacetime. The top tax rate rose by 150%, real federal spending rose by nearly 100%, and federal spending as a percent of GDP rose by nearly 150%.

And given the prescriptions liberal economists, journalists, and policymakers have been pushing since 2009—more taxes on the rich and more government spending—well, Hoover has already generously given us all the greatest experiment in American history of that very same prescription; by ballooning the federal budget and soaking the rich. Was the result an energetic recovery achieving full employment in record time? No, it was the Great Depression; delivering peak unemployment rates double that of the nearest slump (also the Depression of 1893) and lasting two-and-a-half times longer than the next longest downturn (tie: Depression of 1873, Depression of 1893, and 2008 Great Recession—as measured by number of years to return to full employment).

So what’s our Great Depression’s great lesson for this month? More government spending makes recessions longer and worse (for a modern-day example, see Japan’s nearly three decades of government stimulus spending). Multiple articles have been written about the Hoover myth and the real lessons of early 1930’s fiscal policy, but they have been confined mostly to conservative and libertarian outlets such as the Mises Institute, CATO, and Mercatus Center. Most of America simply isn’t aware that Hoover the tightfisted miser is a complete myth, because if you watch or read mainstream media you’d probably never know either.