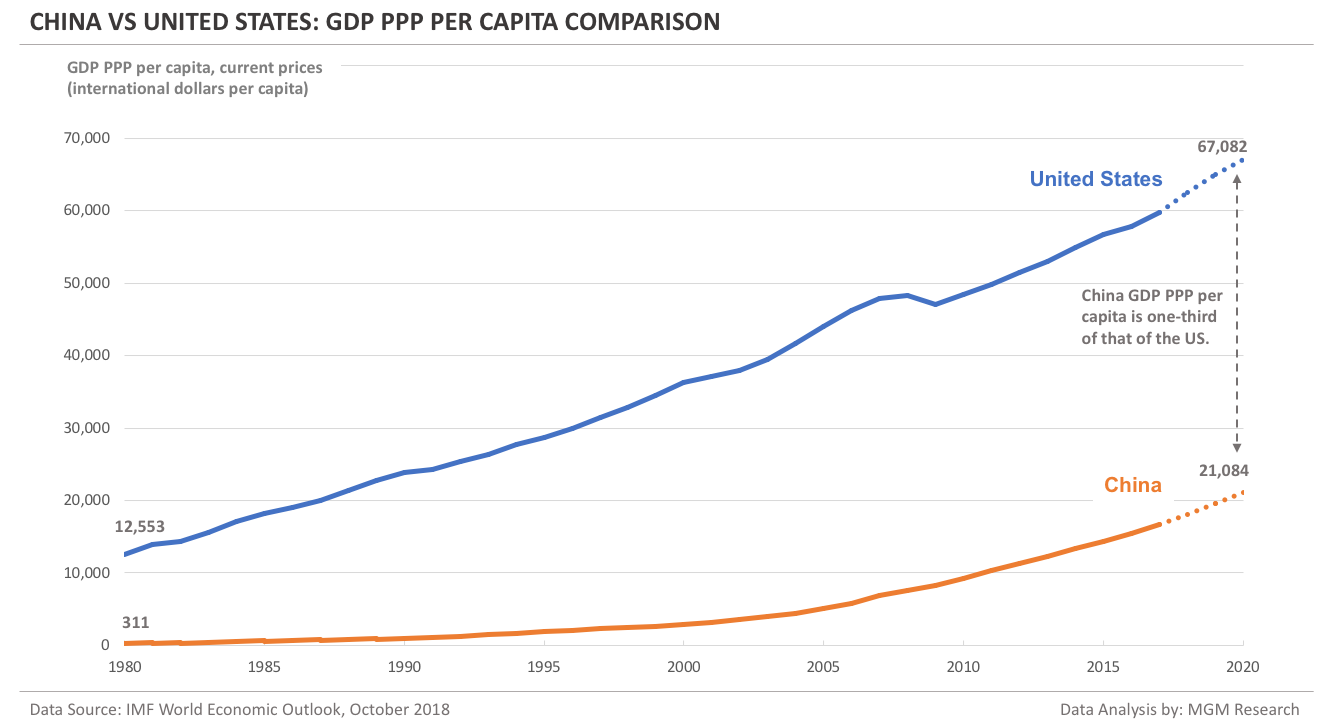

Click here to read the original Cautious Optimism Facebook post with comments

3 MIN READ - A national debt update from the Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff.

Cautious Optimism regular Keith Shapiro (aka. K-Shap) commented a few weeks ago that “governments love inflation.”

He’s absolutely right and here’s a prime example of why.

This November the federal government will have repudiated $5 trillion of its debt since Joe Biden took office, but without paying the debt down by even a penny. It will all be through the magic of inflation.

Here’s the fairly simple math.

1) Starting with the arbitrary baseline of January 2021, the national debt was $27.75 trillion at the time.

Since January 2021 the CPI index has risen 19.9%—diminishing the dollar by 16.6% of its value. Hence, $4.61 trillion of the $27.75 trillion debt has been wiped out due to the watered down value of our money.

(We are using official government CPI here for what it’s worth, so apply your own numbers which will certainly mean higher inflation and ultimately far more than $5 trillion of debt erased)

2) In 2021 the federal government added another $1.87 trillion of debt and the dollar has lost 10.3% of its value since then.

Another $193 billion of debt erased.

3) In 2022 the federal government added another $1.80 trillion of debt and the dollar has lost 4.6% of its value since then.

Another $83 billion of debt erased.

4) In 2023 the federal government added another $2.58 trillion of debt and the dollar has lost 1.6% of its value since then.

Another $42 billion of debt erased.

We’ll skip what debt has been added so far in 2024.

So add $4.61 trillion + $193 billion + $83 billion + $42 billion and inflation has helped the Treasury renege on $4.93 trillion of debt.

These numbers are as of September 2024. Unless the government borrows nothing in the next two months and inflation reaches zero as well, the amount of debt relief the government has granted itself will exceed $5 trillion by November.

As a reminder, $5 trillion is roughly how much George W. Bush increased the national debt during his eight years in office—a figure liberals screamed bloody murder about at the time. But with less than four years of inflation the Federal Reserve has just “coincidentally helped” absolve Bush’s entire eight-year debt tab just by cranking up the printing presses.

It’s an old trick that goes back to (the oldest version the Correspondent can find) ancient Greece around 380 BC. Cautious Rockers who missed that story can go to…

https://www.cautiouseconomics.com/2024/02/economic-history-05.html

The same story repeated itself in ancient Rome…

https://www.cautiouseconomics.com/2023/07/inflation-currencies33.html

And in medieval England…

https://www.cautiouseconomics.com/2022/10/inflation-currencies25.html

And today across the entire world with modern central banks.

Governments borrow $1,000 and promise to pay it back 10 years later. But in between the economy grows 2% a year and the central bank raises prices by 2.5% a year, so 10 years later nominal GDP is 56% greater.

Assuming the government taxes roughly the same percentage of GDP in 10 years that it does today, its nominal revenues are 56% higher, making it easier to repay the $1,000.

Of course the economy really only grew 21.9% in those ten years (1.02^10). The other 34.1% of that nominal GDP growth is simply inflation and higher prices.

It’s a sweet deal for the government that finds it much easier to repay debt with considerably less valuable dollars that are more abundant when the bill comes due.

But there’s no such thing as a free lunch. So who really pays for this sweet deal?

Savers—basically anyone holding dollars who watches their wealth debased 22.4% by the printing press.

In a longer 30 years their dollars are debased by 53.2%. Yep, cut by more than half.

This is what the Fed calls “price stability,” and what Democratic politicians pin on “corporate greed.”

And these numbers all assume a scenario of 2.5% inflation. We saw official inflation peak at 9.1% in late 2021.

The 1970’s were even worse. From 1971, when Richard Nixon broke the last link between the dollar and gold, to 1983 the dollar became 38 cents wiping out savers and retirees in particular. If the national debt ever starts to get unmanageable the Fed can come to the Treasury’s rescue in such a manner again (imagine our $35 trillion debt becoming only $13.3 trillion in twelve years), then officially announce “Sorry, it was just a small mistake on our part. We have inflation back down to about 2% so everyone should be happy now.”

And anyone who complains that “Hey, this fiat money monopoly run by the Fed is ripping us all off. We need money tied to a finite commodity like gold again” will be mocked and ridiculed by the liberal media and government economists as a pedantic neanderthal.

Because everybody knows the only way an economy can possibly function is with a state-sanctioned monopoly that creates money at zero cost without limit, gets its power from the same government that is heavily in debt and which uses police and guns to shut down any alternative form of money while forcing its citizens to use only its crummy, depreciating currency.

Another coincidence: the government and its economists say the state monopoly issuing their constantly devaluing money is just the only version of money that will ever possibly work. We can't even think about alternatives.

{kind=link}

{kind=link}