Click here to read the original Cautious Optimism Facebook post with comments

8 MIN READ - The Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff continues explaining how he can actually suck it up and tolerate living in the workers paradise: the People’s Republic of San Francisco—this time devoting an entire column to San Francisco’s housing crisis.

In Part 1 I explained how certain backwards San Francisco policies are making problems like homelessness, syringes, human poop, shoplifting, store closures, car breakins, and business/job departures worse, and how as Economics Correspondent I’m lucky enough to be mostly unaffected by these policies. That’s at:

http://www.cautiouseconomics.com/2021/11/short-bites-18.html

Part 2 will be dedicated exclusively to San Francisco’s three-plus decade long housing crisis where home and rental prices have relentlessly spiraled out of reach for a greater and greater share of residents… most of whom still keep voting for the same policies.

HOW IT STARTED

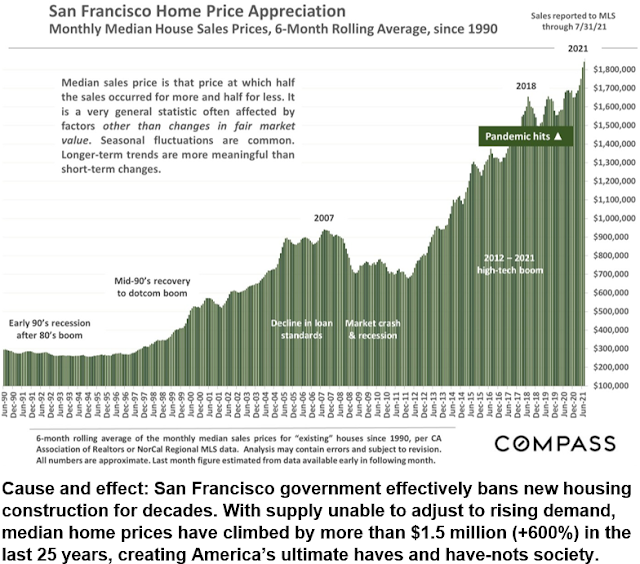

First let’s review how San Francisco housing became a disaster to start with.

The City is already pretty small, surrounded on three sides by water, and is already a hotly desired living area due to its natural beauty and other urban amenities. So San Francisco housing prices have traditionally been higher than the rest of the country.

However in the 1980’s the increasingly progressive politicians and voters decided it would be best to prohibit building virtually all new housing. The one exception was a small enclave east of the South of Market District (SOMA) but that supply venue was so small it did nothing to offset what was effectively a citywide ban on new construction.

The forces behind the ban were a strange-bedfellows alliance of interest groups.

1) Standard liberal voters who considered it evil that developers can make a profit building houses so best to stop homebuilding altogether.

2) Homeless advocates who decided “If you’re not going to give new housing away for free to the homeless then we’ll make sure no one else can have it either.”

3) Conservationists who didn’t want to see anything that looked like a modern structure built anywhere in the City.

4) Wealthy high rise or hillside residents who paid for stunning views and didn’t want to chance another building going up beside theirs and blocking their scenery. In fact, city ordinance has long prohibited hotels in the Fisherman’s Wharf tourist area from exceeding five floors so as not to disturb the views for wealthy residents up on Russian Hill overlooking the Bay.

5) Homeowners in general who liked the idea of blocking new construction which effectively cartelized the supply of existing housing and drove their home values up faster.

Well standard freshman microeconomics informs us when government freezes the supply of housing—making it “inelastic” as economists say—and the demand for housing rises due to population growth, inflation, lower interest rates, and increasingly wealthy international buyers, prices for both purchase and lease will skyrocket.

And they have. Today San Francisco’s median home price has reached $1.85 million, a sevenfold increase over 25 years.

Today only a tiny minority of the wealthiest can afford home ownership with the masses condemned to eternal renting.

With such a small minority of wealthy citizens owning an asset that continues to rise rapidly in value and everyone else shut out, San Francisco has become a shining example of haves and have-nots, a pejorative that the local liberals love pinning on free market conservatives. Yet despite all their virtue-signaling about the Republican evils of inequality, San Francisco’s progressive voters and government have created a societal GINI inequality coefficient higher than Nicaragua, Sudan, Congo, and Cameroon.

Another irony is San Francisco liberals routinely accuse conservatives who oppose high taxes and wealth redistribution of having an “I’ve got mine, now F-you” attitude.

Free market conservatives of course really think “I earned mine. Now you earn yours instead of using government to steal from me.”

But the great irony is that “I’ve got mine, now F-you” is precisely how San Francisco homeowners operate. Once they navigate into home ownership they lobby government to block any more homes from being built which is truly shutting out the underprivileged and telling them to screw off.

Or as Dennis Miller likes to say: “A developer is someone who wants to build a house in San Francisco. An environmentalist is someone who has a house in San Francisco.”

LIBERALS BLAME CAPITALISM

For nearly four decades as San Francisco voters and city government have refused to allow new housing construction, they’ve all universally condemned rising prices—except for existing homeowners who love it.

I remember a developer who actually penetrated pretty far into the obstruction process back in the mid 2000’s. The city government had placed an unrealistic barrier of “X-percent of all units must be sold at below market price” (I can’t remember the exact number, it may have been around 15 or 20 percent) which had effectively deterred new developers while giving the Board of Supervisors culpable deniability, arguing “Of course we allow new housing. We only require developers to meet their obligations to society's underprivileged.”

Well when that developer unexpectedly agreed to the terms the Board of Supervisors was caught off guard and quickly scrambled to raise the requirement at the 11th hour. Once again I can’t remember the exact number but it was something dramatic, akin to doubling the percentage of units that had to be sold at “below market.”

The developer, who had already sacrificed plenty to get permission to build in the City, balked at what was now a moneyloser and walked away. The Board of Supervisors cheered and high-fived, San Francisco liberals declared victory, and both went back the next day to complaining about high housing prices.

I've seen multiple ballot proposals to approve new housing construction projects in the City over the years and virtually all of them have been killed by the voters.

Another side-effect of BANANA policies (Build Absolutely Nothing Anywhere Near Anyone) is gentrification.

As prices skyrocket all over the city buying homes in once unthinkable poorer neighborhoods becomes an only remaining option for higher-income workers. But once they start buying prices are driven up to a level that the poor can no longer afford. Gradually higher income (ie. usually white and Asian) residents move in, displace the old guard, and the newly arrived money leads to a once dilapidated neighborhood getting a revitalized upgrade.

But inevitably the ethnic “diversity” of the neighborhood is watered down and liberals protest that “San Francisco is becoming a whites-only city.”

The next step then is to blame racism—in the most left-wing, progressive city in America—when in fact a ten-year old can see gentrification is the inevitable “pro-white” economic consequence of their own interventionist, anti-development policies.

All throughout I’ve been amused by the online commenters who then blame “free market capitalism” and “corporate greed” for skyrocketing home prices and all these other outcomes.

We’re talking about the most heavily government-controlled housing market of any large city in the United States, and a city government blocking virtually all attempts to build new houses—while sanctimoniously declaring “housing is a human right”—somehow serving as an exemplar of free market capitalism. It's akin to calling Joseph Stalin’s gulag archipelago labor camps “the logical outcome of the Soviet free market system.”

When confronted with the objection that artificially constrained supply is what’s driving unaffordability, not imaginary free-market capitalism, the locals often drum up a standard next excuse: “Well there’s no land left to build on anyway.”

Aside from the fact that San Francisco still has plenty of empty lots, abandoned buildings, and other plots available for sale to rebuild on, there’s also the option to “build up,” an idea that former Mayor Gavin Newsom made a half-hearted attempt to champion, but he was repeatedly squashed by the always-more-leftist Board of Supervisors.

To which the lefties then object “But we want San Francisco to stay charming. We don’t want to look like Hong Kong or Blade Runner.”

OK, I understand that sentiment although I don’t think it gives anyone the right to stop someone from building a house in the middle of an affordability crisis.

But even if you accept the “government should block new housing to keep San Francisco charming” premise, then why do they still 1) complain about rising home prices which they've created, and 2) blame "capitalism?"

Part of being an adult means accepting the consequences of your actions and admitting responsibility, a concept that’s pretty much been lost here for at least half a century.

On a positive note, a few years ago former Mayor Ed Lee did manage to outmaneuver the Board of Supervisors and get some limited new construction approved during his tenure. And in the last few years I’ve seen some new, larger scale construction go up near the Van Ness corridor and around Twitter headquarters.

Ed Lee died unexpectedly of a heart attack one night shopping at Safeway but his successor, current Mayor London Breed, has promised to continue his policies.

But San Francisco is more than 30 years and over 300,000 housing units behind the curve. The rate of new construction is barely enough to keep up with new demand, let alone make up for over three decades of inaction. So my personal prediction is prices will continue to rise—albeit not as rapidly as before—and the local lefties will exclaim “Aha! You see? They’re building new housing and prices are still rising. Government was never the problem!” (eye roll)

HOME OWNERSHIP: OK, NEVER REALLY AFFECTED ME

So how does this disaster not affect me personally?

Even when I moved to San Francisco home prices were already out of reach so I arrived expecting to be one of the City’s many “lifetime renters.”

And even if you’re rich enough to make the down payment and qualify for the mortgage on a median priced home ($1.85 million) there are still lots of other problems.

With such a huge mortgage to pay—$12,250 a month PITI on a median priced home with 10% down and a 3.5% 30-year loan—all it takes is one untimely job loss to put homeowners in desperate straits.

It’s one thing to keep paying a $3,000 mortgage while the government pays you $2,000 a month in unemployment. $12,250 is another matter entirely that can bankrupt anyone in a matter of months unless they have a lot of savings available to burn through.

The property taxes are still high. Yes, Proposition 13 capped the annual tax rate at 1.2% back in the 1970’s, but on a $1.85 million home that’s still $22,200 in annual property taxes alone.

San Franciscans love to take out their frustrations by looking for things wrong with conservative Texas and criticize the Lone Star State for its roughly 2.8% property tax rate (they fail to mention there's zero income tax in Texas), but the same $1.85 million home might cost $350,000 in Houston… and a 2.8% property tax on a $350,000 home is $9,800—a lot less than $22,200 in San Francisco.

BTW in my district $1.85 million will get you three or four bedrooms and anywhere from 1,800 to 2,200 square feet. You’ll either get one floor of a "tenancy-in-common" (aka. TIC) building or your own tiny house directly attached at the sides to others (see photo).

Then there’s earthquake insurance. No private insurers are willing to take that risk on their own since a catastrophic quake that destroys the entire Bay Area would bankrupt them. So mortgagees mostly buy earthquake insurance from the California Earthquake Authority (CEA), a state agency. Although the CEA is funded by a consortium of private insurers, the funds and policies are managed by the state office.

Now I’ve never had to buy a CEA policy, but they’re famous for being incredibly expensive with as basic coverage as you can get on fairly lousy terms—but still required by many mortgage investors.

And if such a megaquake ever really struck there’s a huge question mark hanging over whether the CEA would actually be able to pay out, how long it would take, and how slow the catastrophe response and claims payout would be.

Perhaps we have some California homeowners here in CO Nation who live in earthquake zones who can provide more details on how their CEA policy works.

Also San Francisco homes tend to be very, very old—many over 100 years old. My own building was constructed in 1912.

While this makes for interesting architecture and beautiful neighborhoods—after the human poop and syringes are powerwashed away—you can imagine the cost of upkeep and repair for so much outdated/ancient plumbing, electrical systems, heating, construction… you name it.

So there’s lots of reasons not to stretch yourself too thin to buy a house in San Francisco. Unless you’re truly megawealthy with millions of dollars in the bank and can afford to be nickeled-and-dimed to death—with $5,000 and $10,000 nickels and dimes.

ps. Speaking of needing megawealth I've learned that Julia Roberts recently dropped $8.3 million for a Presidio Heights home about nine blocks from my apartment. See photo:

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.