4 MIN READ - The Cautious Optimism Correspondent for Economic Affairs and Other Egghead Stuff was particularly impressed by this article’s thesis (“an economy starved of savings has little resilience to any shock”), but more for its financial insights than its traditional Austrian capital insights which he’d like to criticize oh so slightly.

Read FEE.org article here:

https://fee.org/articles/generations-of-keynesian-policies-have-made-us-extremely-vulnerable-to-the-covid-19-economic-crisis

For those not familiar with Austrian Business Cycle Theory (ABCT), the act of saving one’s income—which means deferring consumption—preserves a share of the real physical economy to be channeled towards producing capital tools and machines that enable greater production and higher standards of living in the future.

The article opens with the first of two major insights by establishing that when consumers spend all their income and more, they are signaling to businesses to focus more on producing goods for immediate consumption and less on producing capital goods that increase output per worker in the future. And over time sustained overconsumption leads to slowing economic growth as “seed corn is eaten.”

ABCT also argues that when central banks force interest rates down, they discourage saving and encourage more borrowing and consumption. Thus fewer capital goods are produced and the artificially low interest rate actually slows economic growth over any time frame beyond the short-term cheap money “sugar rush.”

There are more nuances to ABCT but the Economics Correspondent will stop there and say he generally agrees with the theory.

However the key economic disruption in the coronavirus economic crisis is not insufficient capital goods leading to meager gains in productivity.

Even if factories were flush with more modern capital tools and machines, the economy would still be in the hole now because government lockdowns and the virus itself are interfering with the ability of human workers to cooperate and employ those machines efficiently—not to mention managerial planning, maintenance of capital machines, distribution of intermediate and final goods and services, and the ability of end consumers to purchase them or take delivery.

Which leads to the second and stronger insight of the article regarding the Federal Reserve’s policy impact on the economy’s financial health.

It’s no secret that nearly a decade of zero interest rates has encouraged debt, debt, and more debt—taken on by firms, households, and governments.

Companies have leveraged to the hilt, floating huge debt offerings not only to finance expansion, but also to buy back stock.

https://fred.stlouisfed.org/graph/fredgraph.png?g=qVLI

{kind=link}

While the Economics Correspondent has no objection to share buybacks per se, the zero interest rate environment has incited more financially irrational buyback schemes.

For example, paying a cheap 3.5% on corporate notes to raise cash to buy back shares that pay dividend yields of 4% might seem like a perfectly logical move to a CFO except that debt markets would never buy the notes at 3.5% to begin with were it not for Fed interest rate manipulation. Hence the unnatural math has spurred higher risk and higher corporate debt loads.

Borrowing to buy back shares also deprives firms of financial flexibility during a slump. When the music stops suddenly—as it has now—a company can suspend those dividend payments to preserve cash, but it can’t stop paying interest on the debt or refuse to repay it which would lead to bankruptcy.

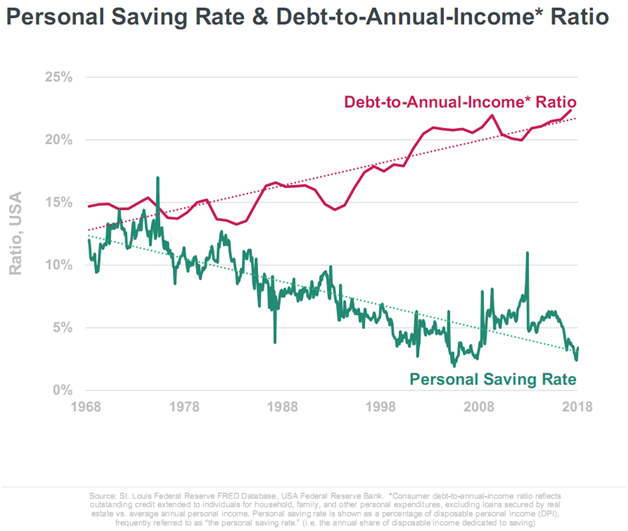

Households have racked up record debt since 2008 as well. Although household debt as a percent of GDP is slightly lower than in 2008, household debt as a percent of household income is once again at a record. And just as importantly the gap between household debt and personal savings has never been greater.

https://www.bourbonfm.com/sites/default/files/users/PatrickBourbon/Personal%20Saving%20Rate%20%26%20Debt-to-Annual-Income%20Ratio.png

{kind=link}

And of course there’s the government’s highly publicized national debt and debt-to-GDP ratio. After rising rapidly from 2009, the debt-to-GDP ratio stabilized somewhat in 2014 around 100% and has set new peacetime records slowly ever since, but that stabilization is about to change very soon for the worse.

https://fred.stlouisfed.org/series/GFDEGDQ188S

The Economics Correspondent predicts the national debt will very soon eclipse the all-time record debt-to-GDP ratio of 120% set during World War II.

All of these record levels of debt and low savings are the result of a central bank that forced interest rates to or near zero for over a decade. With such low rates the public would be crazy not to borrow and consume, and just as crazy to save—except for the highly disciplined few willing to stomach paltry returns and save anyway.

Which brings us to the crisis. Suddenly firms, households, and governments don’t see much income coming in. We’ve all been forced to hunker down and, even when that ends, will mostly still keep hunkering down voluntarily until the virus problem is unequivocally resolved.

A society that had accumulated ample savings—both corporate and household—would have a cushion to ride out the storm. It would be painful, but it wouldn’t have to be desperate, at least in the short-term.

But thanks to the Fed few firms and households found themselves in that favorable position in March when the crisis erupted.

The result is companies are scrambling to borrow even more to build that cash cushion (with the Fed accommodating them yet again), many that were previously overleveraged are going bankrupt, and households and small businesses—which unlike corporations have few capital assets to pledge as collateral—are left dependent on unemployment checks and government assistance since they have little savings to get through the slump.

Even the federal government doesn’t have the money and has to borrow to, among other things, bail out highly indebted state governments.

And why didn’t they have a cushion? Keynesian economic policies.

Central banks believed before and after the 2008 crisis that economic recoveries should be “stimulated” with record low interest rates that ultimately produced record levels of indebtedness. Ironically the Austrian criticism argues that super low interest rates lead to slower growth and slower recoveries over the longer term because the economy is starved of savings and deprived of real physical capital.

And the attached FEE article is dead on right that America’s companies, households, federal and especially state and local governments are in a far more desperate financial position now because of the Keynesian monetary policies of yesterday.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.